Economics

First thinEconomicsg’s first: there’s been no “rise and fall” of economics. And no clickbait here! The truth is that more than once (on one occasion, a fateful first meeting with a potential suitor, who has now gone down in infamy among my girlfriends for this unfortunate exchange) I have found myself face to face with an individual who has been aghast (!) by my interest in the field. Assuring me that economics is a manmade construct, that is soon to be on the way out. Or worst yet that I’m some loathsome conservative/liberal, a hungry capitalist whose greed will destroy life as we know it….!

Economics is a field of study. It’s not a political affiliation, nor does it identify a particular type of economic system (for example, capitalism or socialism are types of economic systems). Yes, patterns between variables have been identified, we’ve come up with (SOME! not all) theories that are hard to prove, and many (MANY!) economists are regularly mistaken about economic forecasts. BUT, economics is the study of how people, institutions, and society make choices under conditions of scarcity (Yes, that’s taken straight from my Econ 120 textbook; Essentials of Economics, Third Edition; Brue, McConnell, Flynn, McGraw-Hill, 2014). Economics is a science. Just like chemistry and biology, though more closely aligned with the social sciences of psychology and sociology. There’s a great piece written by 2013 Nobel Laureate, Robert Shiller about economics and its place in science.

Over the years, I’ve gotten into many discussions about economics; everything from why people don’t pay for Friday night fireworks in Waikiki to the truly disastrous American food supply system (let’s just say you don’t have nearly as many choices, as there are only a few major players who control nearly all widely accessible products at popular grocers).

Supply & Demand: A love affair

The one topic that seems to unite people in recalling their Intro Econ course is…SUPPLY AND DEMAND! I know that I’m revealing my inner nerd (if it’s not been totally apparent already) but really, nothing makes people laugh and grimace quite like trying to get their graph just right. So, although that title might be a bit scandalous at first read, I can assure you, it’s actually quite accurate (when talking about the slopes of these lines, not so much the concept of economics).

Economic principles are statements about economic behavior or the economy that enable prediction of the probable effects of certain actions*. Eventually, we are going to go so far into the weeds on that topic, it will blow your freaking mind. But for now, we’re going to accept its veracity in order to begin building our supply and demand graph.

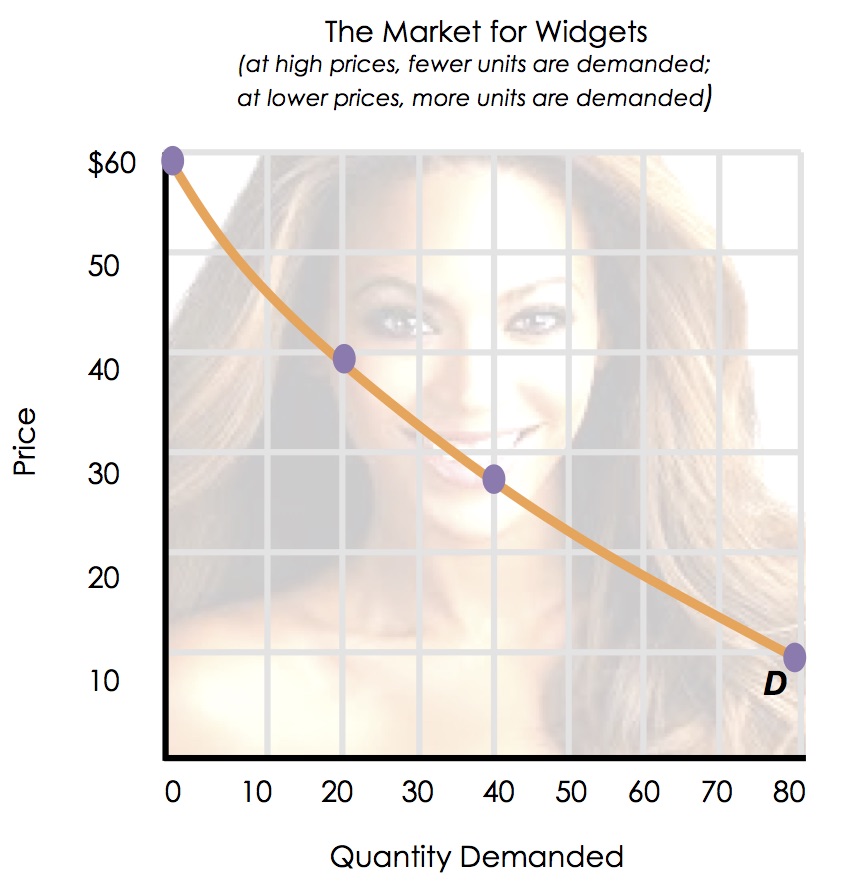

The Law

Using the above ‘economic principle’ definition as a guiding light, it’s safe to say that if a product is incredibly expensive (barring any other considerations, such as personal preference), people will buy fewer.

Let’s say that you can spend $100. If given items are priced at $25 a piece, you can only get four. If the price is only $2 for each item, you can buy 50! In this way, we can imagine the demand curve: you buy a few if the price is high (not considering any other factors), buying subsequently more goods as the price decreases.

As promised, the result is totally, 100%, absolutely logical:

Law of Demand: all things equal (yeah, it’s a bit of a copout…we’ll discuss), as the price falls, the quantity demanded rises, and as the price rises, the quantity demanded falls.

#queenbey

And because you can’t have the “fall” without the “rise”…next up: the supply curve [link with article explaining new articles come out every Tuesday]

{kind=link}

To understand Supply & Demand curves, which you nicely relate to a lot of real-life decisions, seems like you also need some basic understanding of stats! 🙂 – DA